The Different Kinds of Utilities

Electric power probably has the most fragmented structure of any industry.

There are three basic functions on the grid: generating power, transmitting and distributing it, and selling it to end customers. Some utilities do all three. Some do one or two. And some do none! (I’ll get back to this.)

And utilities have many different types of owners. Investor-owned utilities (IOUs) are generally publicly traded companies. There are non-profit utility cooperatives (co-ops), and there are utilities owned by federal, state, municipal, and other government entities.

And these utilities have different market postures. There are “poles and wires” utilities (TDUs) that own transmission and distribution but never take ownership of the power they transmit. The utilities that do own power either get it by generating it or by buying it wholesale, and they sell it either on the wholesale market or to end customers (retail). You can imagine this as a 4x4 matrix, and there are utilities in every quadrant.

And every state has a mix of utility types, postures, and ownership types. A state’s mix reflects its geography and political history. Because the power grid has been around so long, it’s passed through and been changed by a succession of political orders. Because the power grid involves so much connected physical infrastructure, reforms typically build around rather than replace the old order. And because the power grid is primarily regulated at the local and state levels, different reform movements have penetrated to different degrees in different places.

This is what gives the grid its complexity. I’ll now try to cut down that complexity and get the lay of the land. Let’s start by comparing three states that represent the three market structure regimes: Florida, Tennessee, and Texas.

Florida represents the first era of utility regulation. The first utilities were owned by investors and/or municipalities. Today, 68% of the electricity consumed in Florida is generated by investor-owned utilities (IOUs) and 10% is generated by municipally-owned utilities (munis).

Most IOUs and munis were founded in the late 1800s and early 1900s. They have names like “[City] Power & Light” or “[city] Utility District”. Electric utilities were just one of many new industrial-era companies building linear infrastructure with monopolistic network properties. There were also railroads, telegraphs, and oil and gas pipelines. In the Progressive Era, states established commissions - with names like the “Public Utility Commission”, the “Public Service Commission”, or “Corporations Commission” - to regulate these industries as public utilities. Electric utilities were given geographic monopolies as vertically-integrated owners of generation, transmission, distribution, and retail marketing. Florida’s three IOUs still have retail and transmission monopolies.

In Florida, some large cities like Jacksonville, Gainesville, and Orlando generate most of the power that they consume, but dozens of cities produce no power and instead buy it wholesale, only managing the distribution system and the retail marketing. Munis typically buy their power from IOUs and IPPs. Florida is unique for having the Florida Municipal Power Agency, which generates power and sells it wholesale to member munis.

This graph shows the market posture of all the utilities in Florida. In the top right are IOUs and large munis that mostly generate their own power and sell directly to consumers. In the top left are the two major wholesale utilities. The Florida Municipal Power Authority is a muni that generates power and sells it wholesale to the smaller munis in the bottom right corner. These smaller utilities own distribution (and sometimes transmission) and sell the power directly to consumers, but don’t generate it themselves. And the Seminole Electric Cooperative is similar, but it sells to co-operative utilities (co-ops). These retail-only utilities might also buy power wholesale from IOUs and independent power producers (IPPs).

I haven’t explained co-operative utilities or IPPs yet. They’re not a major force in Florida, generating 4% and 18% of power, respectively. These forms of utilities came along later in history and penetrated Florida to a lesser extent than other states. To explain them, let’s move forward in time.

The next force that majorly shaped the electric power industry was the New Deal era. During the New Deal, the federal government got into the business of generating power (e.g. building the Hoover Dam) and of being an electric utility. That brings us to Tennessee.

In Tennessee, 85% of power is generated by the Tennessee Valley Authority (TVA), a federally owned utility created by Congress in 1933. The TVA sells all of its power wholesale to several dozen municipal and co-operative utilities that own distribution lines and sell power to end customers.

The federal government had a natural role to play in the early days of electric power because hydroelectric power was a popular generation technology and most rivers are managed by the federal government. At the same time electric power was taking off, rivers were being dammed for irrigation and flood control by the U.S. Bureau of Reclamation and U.S. Army Corps of Engineers. Adding hydroelectric power made perfect sense.

During the Great Depression, Congress appropriated unprecedented funding to public works in a series of economic relief acts. Dam and hydroelectric construction accelerated. At the same time, there was enormous backlash against IOUs as many retail investors had lost their savings in a massive mania in utility stocks. Among other reforms, the government became an active player by establishing four principal federally-owned utilities. The TVA is by far the largest.

Although power generation in Tennessee is highly concentrated, the retail sale of power is divided between 82 utilities. While TVA sells 87% of its power wholesale, it does have some retail contracts with large federal customers (e.g. national labs, military bases, etc.) and large industrial customers (e.g. aluminum smelters). The rest of retail sales are split between munis (57%) and co-ops (24%).

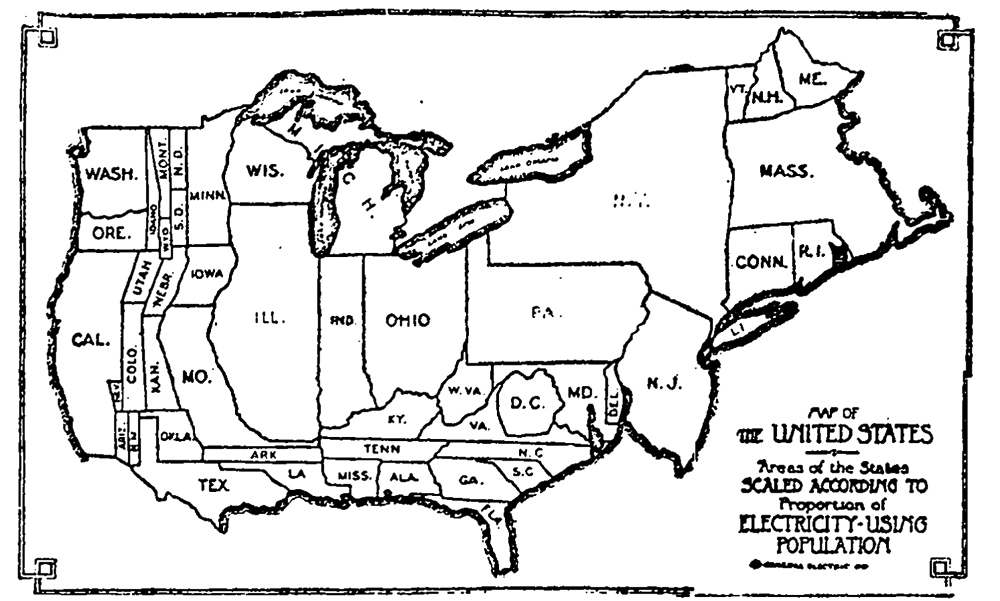

Co-operatives were also established during the New Deal to provide power in areas too rural for IOUs or munis. In the mid-1930s there were still massive stretches of territory with no electric power, especially in the South where Roosevelt’s support was strongest. This 1921 map scaling states by the proportion of the population with electricity service shows how limited electricity was to the industrial Midwest and Northeast.

So Congress passed the Rural Electrification Act in 1936 to give loans to establish electric cooperatives. Today there are 604 co-ops, with the highest concentration being in states with more rural areas.

There are basically two kinds of co-ops: distribution co-ops and generation & transmission co-ops. Distribution co-ops own distribution lines and sell power to end customers, but they generate no or very little power. They buy power exclusively from generation & transmission co-ops (G&Ts), which are like a wholesale version of a co-op. They don’t sell to end customers. They sell only to their distribution co-op members, and they own the transmission lines to reach them. G&Ts vary in how much they generate of the power they sell. In the bottom left corner there are G&Ts that don’t generate any power but instead act as a buyer pool and a trading desk for their members.

Where do they buy their power from? I suppose they could buy from anyone, but probably most commonly they buy from IPPs and on managed spot markets.

During the 1970s energy crisis, a number of energy reform laws were passed, including the Public Utility Regulatory Policies Act of 1978 (PURPA). PURPA created small exceptions to the utilities’ generation monopoly, allowing non-utility companies to own power plants and to sell their power to utilities under long-term agreements. Over time, the exceptions grew, but the IPP industry was limited by the fact that it faced a market of a small number of buyers who regarded them as competition.

During the Neoliberal era, the IPP opportunity expanded with the creation of Regional Transmission Operators (RTOs). An RTO is a regional grid that both ensures the physical stability of the system (e.g. that load and generation are balanced and that transmission lines aren’t overloaded) while managing a spot market for wholesale power and dispatching power plants in the RTO accordingly. Utilities in RTO territory would have to buy power from the wholesale market. Instead of negotiating long-term bilateral agreements with utilities, IPPs could now sell directly into the wholesale market.

RTOs were eventually established in most of the country and today they cover two thirds of electricity load. Some states not only required the utilities to participate but also required them to sell their power plants to IPPs, reducing them to “pole and wires” utilities (TDUs). And some states allowed for the creation of third-party power marketers who would buy power from the wholesale market and then sell it to end customers, without owning power plants of their own.

That brings us to Texas, the prime example of this competitive model for electricity market structure. In Texas, power generation is dominated by IPPs. In fact, this graph understates the role of IPPs at 87% of generation. Inside Texas’s RTO (ERCOT), the IOUs were turned into TDUs. The three IOUs on this graph are located in Texas but outside of ERCOT. The three remaining utilities engaged in non-negligible power generation are the LCRA (a state-level version of TVA), and two municipal utilities.

Texas is also a state with retail choice. The traditional investor-owned utilities no longer sell power either wholesale or retail. Co-ops and munis still exist, but the vast majority of power purchased in Texas is purchased from retail power marketers.

Nationally, retail competition hasn’t spread as far as deregulated wholesale markets. Electricity retail is regulated at the state level, and some states choose to participate in ISOs/RTOs while limiting retail competition. For example, Indiana participates in the MISO deregulated grid but has no competitive retail, with the minor exception of PPAs that large industrial customers might have with IPPs. While two thirds of load is generated on deregulated grids, only 20.5% ($67.6B) of retail sales were by competitive retailers.

A very large portion of competitive retails sales are in Texas. Retail competition is widespread in Texas because the state ended retail sales by IOUs, forcing their customers to switch to competitive retailers. Other states allowed IOUs to remain in the retail business, and most customers have stuck with IOUs due to simple inertia.

The entity that supplies your power tells you something about the history of its development. If you’re in the territory of an IOU, your city was probably prosperous around the turn of the twentieth century. You probably have a football team for the same reason. If you have a municipal utility, then your city was a city at the time but not a prosperous one. If you have a cooperative utility, then you’re living in a place that was still very rural in the 1930s. And if your power is generated by a a federally-owned utility, then there are probably lots of powerful rivers nearby.